En la imagen

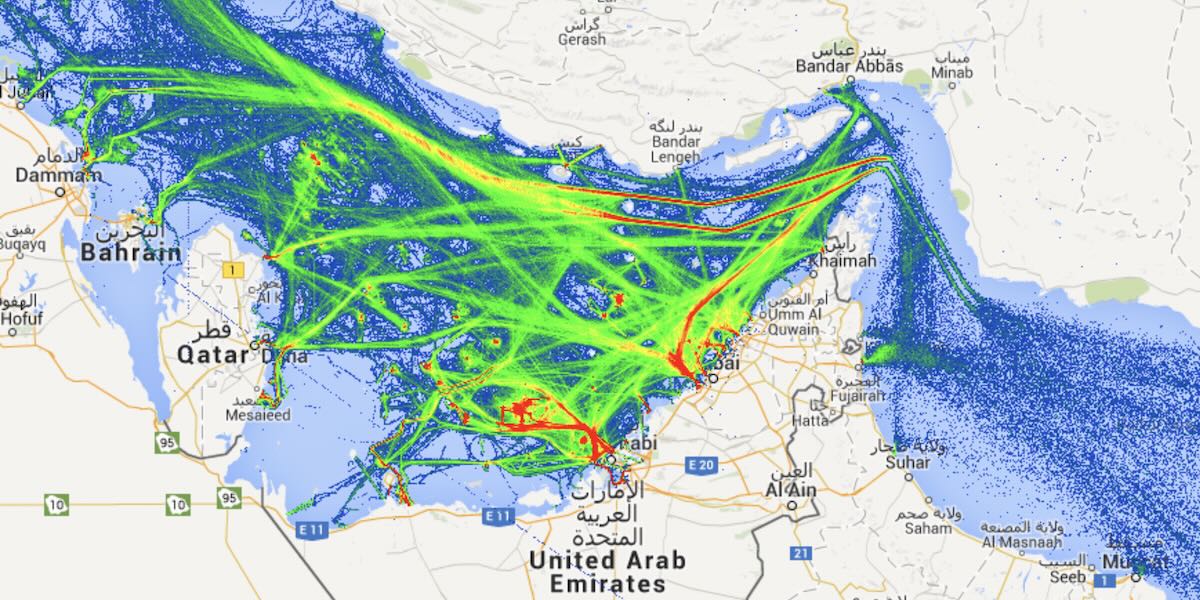

Vessels traffic trough the Hormuz Strait in normal times [marinevesseltraffic.com]

With US military operations in Venezuela and Iran, Donald Trump aimed to control oil production in both countries and, presumably, establish himself as an arbiter of global output and prices, and as someone capable of dictating supply to his competitors. The oil blockade of Venezuela and the attack to remove Maduro from Caracas achieved their objectives, but in Iran, regime change has not been replicated, and this failure has highlighted something Trump hadn’t anticipated: the vulnerability of the Strait of Hormuz due to the lack of an alternative route for exporting hydrocarbons from the Persian Gulf. Trump has discovered that he doesn’t hold all the cards, as he perhaps thought.

President Trump tried to reshape the global status quo with the intervention in Venezuela and the escalation into war with Iran. Nevertheless, the impact of US foreign policy isn’t limited to geopolitics. Both events have been explicitly guided by, and have significantly influenced the international economic situation; particularly the oil and hydrocarbons market. The effects of which are already being felt across the world, with apparently uninvolved countries like Vietnam or South Korea already implementing measures to protect their domestic economies from the fallout of the emerging oil crisis. The consequences of the conflict in the Middle East, which is directly affecting a geographic point through which around 20% of global oil passes through daily, can very easily disrupt the global economy in the long term; especially if the involved parties continue to directly use attacks and disruptions to energy infrastructure as a core part of their strategy.

The OPEC Reference Basket, a weighted average of benchmark crude oil prices produced by OPEC member countries, registered a slight increase in barrel price in February following Trump’s intervention in Venezuela, and a very sharp spike in March due to the ongoing conflict in the Persian Gulf: the basket price jumped to a maximum of $146.05 that month. The situation continues to develop and remains very volatile, but it is possible to extrapolate some conclusions and predictions for the international energy market, and by extension, global economic stability from the events that have already concretely occurred in both Venezuela and Iran.

Venezuela

On the 3rd of January the Trump administration launched a military operation which removed the government of Nicolas Maduro and installed a cooperative administration under Delcy Rodríguez. Since the start, the US administration made it explicit that part of the strategic reasoning behind its actions is the control of Venezuela’s significant but outdated oil industry and use it to achieve both domestic and international economic and political goals. Namely, lower domestic oil prices to $50 per barrel and economically pressure energy markets in favor of American interests and in detriment of hostile states such as Cuba and Iran, and affecting the geopolitical calculus of Russia and China.

As such, one of the first actions of the Trump administration has been to ‘negotiate’ with the new interim government for access to US companies and investment into the Venezuelan oil market as well as US ‘oversight’ over policy and export revenues. This intervention into Venezuela’s oil economy is articulated through the US Treasury’s Office of Foreign Asset Control which has issued a series of ‘general licenses’ that allows US firms to market Venezuelan oil internationally, import into Venezuela goods and services necessary for oil extraction, as well as invest into new and preexisting oil and gas infrastructure in Venezuela.

While the Trump administration states that the sale of this oil must be done at “commercially reasonable terms” in the international market, and that the revenue of these sales which are going to be deposited on a US managed account will be “spent transparently and for the benefit of the Venezuelan people”, this economic plan seems very transparently in the primary interest of the US. Strategically, the vast reserves of underexploited Venezuelan oil could serve as a means to counteract the medium and long-term consequences of the contraction in supply within the US and international markets caused by the ongoing conflict in the Persian Gulf. This already seems to be part of the US administration’s plan since on March 18th the US Treasury further eased sanctions on Venezuelan oil and authorized PDVSA to sell oil directly to the US market, and Trump announced a 60-day freeze on Jones Act to facilitate importation of oil to the US.

Nevertheless, the reality of oil and gas extraction, processing and exportation is that it is a process which requires large amounts of investment into specialized infrastructure and technical expertise which need long periods of time to develop and scale economically. As such, control over Venezuela’s oil has had little to no effect in mitigating the shock and immediate short-term effects of the war in the Persian Gulf.

Middle East

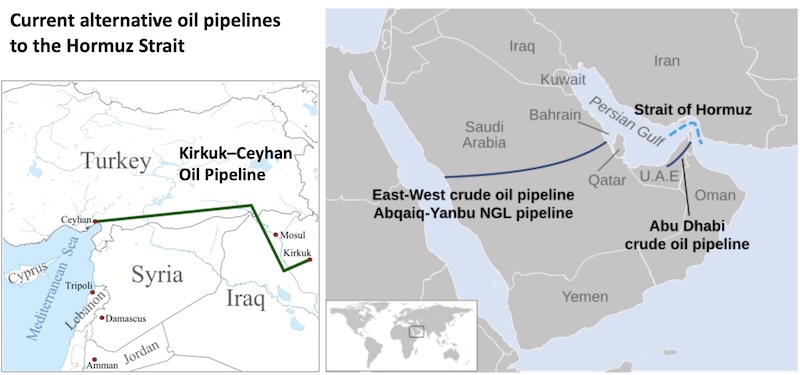

The conflict in the Persian Gulf has had catastrophic consequences for the gas and oil markets internationally because not only does it directly affect some of the world’s largest oil and gas producers, but also, actively has prejudiced and blocked the Strait of Hormuz, which is the main trade artery through which these states export their energy production to the global market.

To illustrate the consequentiality of the situation, Saudi Arabia is the world largest producer of crude oil, exporting $187 billion in revenue from crude oil alone in 2024 and not including refined oil and other oil-derived goods such as chemical products which accounted for well over $40 billion. The UAE, likewise, exported $114 billion worth of crude oil the same year, and over $60 billion worth of other hydrocarbon goods such as petroleum gas and refined oil. Bahrain, for its part, is a major exporter of processed oil and gas products obtaining $5.49 billion revenue from refined petroleum products. In a similar vein, Qatar is a major exporter of the third largest known reserve of natural gas in the world as well as producing around 1.746 million barrels of crude oil per day. On the other side of the conflict, Iran is likewise a major producer of oil and natural gas, having the second largest natural gas reserves in the world after Russia; it is a major exporter of petroleum derived products exporting $1.88 billion worth of ethylene polymers alone in 2024.

All these figures highlight the importance of the gulf states not only directly in the international energy market, but also in the wider global economy as they export substantial quantities of energy and petroleum goods critical for manufacturing nations such as China, India, the US and European states; the disruption of which would have far-reaching consequences. The nature of the current globalized economy has made it so that disruptions to critical points in global production chains in one part of the world have magnified and substantial consequences for economies across the globe. This is already being observed throughout the ongoing conflict in the Persian Gulf.